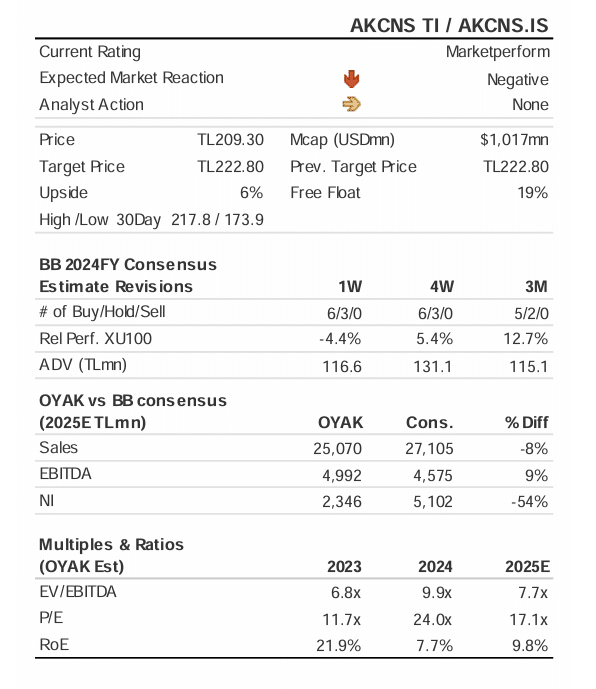

OYAK Yatırım, Akçansa #AKCNS hisseleri için hedef fiyatını 222.8 TL, tavsiyesini “endekse paralel getiri” olarak korudu.

OYAK Yatırım‘ın sınırlı bir yükseliş beklediğini (%6) ifade ettiği Akçansa #AKCNS hisseleri için yayımladığı rapor şöyle:

Weak results on price pressures and low sales

Akcansa announced 24YE net profit of TL1,672mn (-51.1% y/y) and an EBITDA of TL3,774mn (-28.7% y/y), indicating a decent margin of 17.5% (2023: 19.6%, y/y: -2.1bps). Akcansa’s net sales was dropped to TL21,614mn in 2024 (- 20% y/y) mainly on curbed demand through high prices and low exports, while total cement and derivatives sales volume increased by 2% y/y.

Pricing pressure continues

Both domestic and international sales of Akcansa dropped in 2024. In fact, domestic sales dropped to TL17,070mn (- 17.8% y/y), while even more drastic drop occurred in export sales with TL4,429mn (-27.6% y/y). Although sales volumes in cement and derivatives increased by 2%, sales revenues declined due to pricing quotas resulted in below-inflationary price increase in domestic, a slight shift from cement to clinker in domestic market in 4Q24, foreign competitors’ pricing advantages and embargo imposed to Israel.

EBITDA retreats despite lower costs

The drop in costs was mainly due to low energy prices y/y. 20.2% increase in direct labour expenses and 7.6% increase in amortization, on the other hand, softened the slide in COGS. Despite COGS declining by 14.2% y/y, the decline in sales weighed negatively on operating profitability and led to a y/y weak margin.

Net profit decrease on weak EBITDA, financial and deferred tax loss

Beside falling sales revenues, the other reasons for the decline in net earnings are financial loss of TL14mn (2023: +TL243mn), deferred tax loss of TL522mn (2023: +TL49mn) and monetary loss which increased to TL77mn (2023: TL29mn, y/y: +167.4%).

25E estimates, TP and rating maintained

Our 2025 net income, EBITDA and revenues estimates are TL2,346mn, TL4,992mn and 25,070mn respectively. Our target price of TL222.80/share, implying a limited upside of 6%. Akcansa trades fully on 25E P/E of 17.1x and EV/EBITDA of 7.7x.